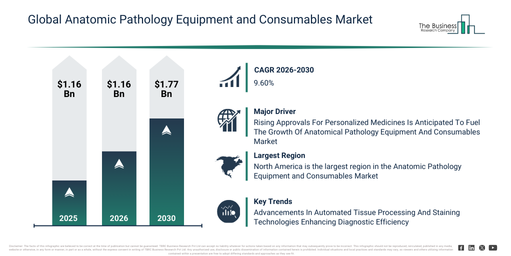

Anatomic Pathology Equipment and Consumables Market Size Projected To Increase From $27.08 Billion To $39.11 Billion During The Forecast Period

Through market attractiveness analysis, total addressable market evaluation, company benchmarking matrices, interactive Excel dashboards, expanded supply chain intelligence, emerging startup coverage, and detailed product insights, The Business Research Company’s 2026 market reports provide more actionable and strategically valuable research.

The field of anatomic pathology equipment and consumables is experiencing robust growth as advancements in medical technology and rising disease prevalence drive demand. This sector plays a crucial role in diagnostics and personalized medicine, making it increasingly important for healthcare providers worldwide. Let’s explore the current market size, factors fueling its expansion, key players, and emerging trends shaping its future.

Steady Growth and Expanding Market Size in Anatomic Pathology Equipment and Consumables

The market for anatomic pathology equipment and consumables has shown significant progress over recent years. It is anticipated to grow from $25.18 billion in 2025 to $27.09 billion in 2026, reflecting a compound annual growth rate (CAGR) of 7.6%. Historical expansion can be linked to challenges such as limited availability of advanced pathology instruments, dependence on manual tissue processing techniques, rising incidence of cancer and chronic illnesses, improved hospital and laboratory infrastructure, and continued use of traditional staining and diagnostic methods.

Download A Free Sample Report For Comprehensive Market Insights:

https://www.thebusinessresearchcompany.com/sample.aspx?id=3410&type=smp

Looking ahead, the market is projected to expand further, reaching $39.12 billion by 2030 with a CAGR of 9.6%. This forecasted growth is driven by increased adoption of automated devices and AI-driven diagnostic tools, higher investments in research and development, growing demand for quality consumables, expansion of clinical labs and research centers, and incorporation of digital pathology and big data analytics. Important trends during this period include greater use of advanced microscopy and imaging technologies, automated tissue processors and slide stainers, more disposable biopsy kits, expanded training and consultation services, and heightened focus on cancer diagnostics and research.

Key Drivers Behind the Expansion of the Anatomic Pathology Equipment and Consumables Market

One significant factor propelling the market forward is the rising number of approvals for personalized medicines. These tailored therapies are developed based on individual patient characteristics such as genetic markers, biomarkers, phenotypic traits, or psychosocial factors that predict treatment response. Anatomic pathology tools are essential in enabling molecular and genetic profiling required for these precise treatments.

Anatomic Pathology Equipment and Consumables Market Regional Outlook: Where Are The Largest Opportunities Located?

For instance, in February 2024, the Personalized Medicine Coalition, a US nonprofit, reported that personalized medicines accounted for more than one-third of new drug approvals by the U.S. FDA in 2023 for the fourth consecutive year. This growth is particularly evident in treatments for rare diseases and cancer, with 26 personalized therapies approved, including 20 new molecular entities and multiple gene and cell-based therapies. This trend toward personalized healthcare is boosting the demand for anatomic pathology equipment and consumables, which support diagnostic testing and targeted treatment approaches.

Detailed Segmentation of the Anatomic Pathology Equipment and Consumables Market by Product and Application

This market is categorized comprehensively by product type, application, and end-use sectors. The product and service segments include instruments, consumables, and services. Applications are primarily divided into cancer diagnostics and non-cancer disease diagnostics. End users mainly consist of hospitals, clinical laboratories, and research institutions.

Breaking down the instruments segment includes microscopes (both light and electron types), slide stainers, tissue processors, cryostats, and embedding centers. Consumables cover reagents and stains, disposable biopsy kits, fixatives and embedding media, glass slides and cover slips, and paraffin wax. The services category encompasses equipment maintenance and repair, training and support, consultation for pathology laboratories, as well as quality control and assurance.

Innovations and Industry Trends Leading to Improved Diagnostic Efficiency

Leading companies in the anatomic pathology equipment and consumables market are focusing on product innovations designed to improve diagnostic precision and streamline laboratory workflows. A key development is the automated tissue processor, which prepares tissue samples for microscopy by automating steps like dehydration, clearing, and paraffin infiltration.

For example, in September 2025, US-based StatLab introduced the Diapath instrument suite in the American market. This line includes the Donatello tissue processor, Giotto stainer, and Galileo slide printer, all engineered to optimize pathology lab operations. Donatello offers customizable protocols with real-time reagent monitoring, Giotto ensures uniform staining through advanced automation, and Galileo provides high-resolution thermal transfer printing for accurate slide identification. These technological advances aim to increase throughput, reduce human errors, and support high-quality diagnostic results.

Competitive Landscape and Leading Players in the Anatomic Pathology Equipment and Consumables Market

Major corporations active in this market include Danaher Corporation, F. Hoffmann-La Roche Ltd., Cardinal Health Inc., PHC Group, Agilent Technologies, Laboratory Corporation of America Holdings, Quest Diagnostics Incorporated, NeoGenomics Laboratories Inc., BioGenex Laboratories, Sakura Finetek USA Inc., Shimadzu Corporation, Bionics Scientific Technologies (P) Ltd, ACMAS Technologies Pvt. Ltd, Labindia Instruments Pvt. Ltd, Hospital Supply Company Pvt. Ltd., Ratek, Leica Biosystem, SORAN, Thermo Fisher Scientific, Becton Dickinson and Company, Epridia, TPL Pathology Labs, ARUP Pathology, Maxdata, Medesa, BMT Medical Technology, Dynex, Medicarom, Hologic Inc., Merck KGaA, Bio SB, Diapath S.p.A., DASA, UW Medicine Pathology, Sunquest, Somatco, ANDAAF Scientific Ltd, and Katchey Company Limited. These organizations are continuously enhancing their portfolios through innovation and strategic partnerships to maintain a competitive edge.

Regional Market Overview and Leading Geographies for Anatomic Pathology Equipment and Consumables

In 2025, North America emerged as the largest regional market for anatomic pathology equipment and consumables. Western Europe held the position of the second-largest regional market globally. The analysis also covers regions such as Asia-Pacific, South East Asia, Eastern Europe, South America, Middle East, and Africa, providing a wide-ranging view of the global market landscape and growth opportunities across different territories.

Get in touch with us:

The Business Research Company: https://www.thebusinessresearchcompany.com/

Americas: +1 310-496-7795

Asia: +44 7882 955267 & +91 8897263534

Europe: +44 7882 955267

Email us at: marketing@tbrc.info

Follow us on:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model