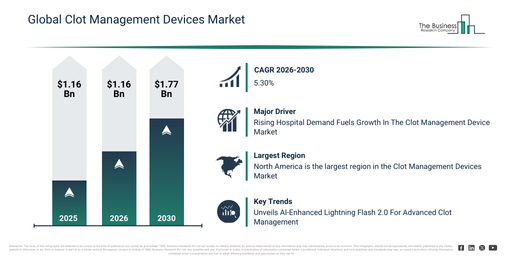

Clot Management Devices Market Set To Grow From $1.92 Billion In 2026 To $2.37 Billion By 2030 At A CAGR Of 5.3%

Delivering more actionable and strategically valuable research, The Business Research Company’s 2026 market reports feature market attractiveness analysis, total addressable market evaluation, company benchmarking matrices, interactive Excel dashboards, expanded supply chain intelligence, emerging startup coverage, and detailed product insights.

The clot management devices sector is witnessing steady expansion as advancements in medical technology and increasing health concerns drive demand. With the rise in cardiovascular conditions and innovative treatment options, this market is set to experience significant developments. Let’s explore the current market size, growth factors, key players, and emerging trends shaping the future of clot management devices.

Clot Management Devices Market Size Showing Strong Growth Between 2025 and 2030

The clot management devices market has seen notable growth in recent years, with its size expected to rise from $1.82 billion in 2025 to $1.93 billion in 2026, reflecting a compound annual growth rate (CAGR) of 6.0%. This growth during the historical period is largely driven by the increasing incidence of deep vein thrombosis and pulmonary embolism, a rising prevalence of cardiovascular diseases, the growth of interventional radiology procedures, expanded vascular care in hospitals, and heightened awareness surrounding clot-related complications. Looking ahead, the market is projected to continue expanding robustly, reaching $2.37 billion by 2030 with a CAGR of 5.3%. Factors contributing to this forecasted growth include an aging population vulnerable to thrombotic events, increased demand for minimally invasive vascular treatments, a stronger focus on early clot diagnosis and management, the development of advanced stroke and thrombosis centers, and broader adoption of endovascular therapies. Key trends anticipated during this period involve greater use of minimally invasive clot removal methods, rising adoption of mechanical and aspiration thrombectomy devices, emphasis on rapid interventions for acute thrombotic episodes, growth in catheter-based treatments for deep vein thrombosis and pulmonary embolism, and a growing preference for retrievable inferior vena cava filters.

Download A Free Sample Report For Comprehensive Market Insights:

https://www.thebusinessresearchcompany.com/sample.aspx?id=15768&type=smp

Rising Hospital Demand as a Key Driver in the Clot Management Devices Market

The growing need for hospitals is playing a crucial role in fueling the clot management devices market. Hospitals serve as essential healthcare centers offering treatment and care for various medical conditions, including clot-related disorders such as deep vein thrombosis, pulmonary embolism, and ischemic stroke. Several factors contribute to the rising number of hospitals, such as population growth, urbanization, expanding healthcare access, aging populations, and the rise of medical tourism. In this context, clot management devices provide effective, minimally invasive treatment options that enhance patient safety and improve clinical outcomes. For example, in May 2024, the American Health Care Association reported that the number of hospitals in the US increased to 6,120, up from 5,129 in 2022. This expansion in hospital infrastructure is a significant growth driver for the clot management devices market.

Core Segments and Breakdown of the Clot Management Devices Market

This market can be segmented into several categories based on product type, device subtype, and end user. The primary product types include neurovascular embolectomy devices, embolectomy balloon catheters, percutaneous thrombectomy devices, catheter-directed thrombolysis (CDT) devices, and inferior vena cava filters (IVCF). Within percutaneous thrombectomy devices, the key categories are aspiration thrombectomy devices and mechanical thrombectomy devices. The neurovascular embolectomy devices segment further breaks down into aspiration embolectomy devices, mechanical embolectomy devices, and embolectomy balloon catheters, which themselves include high-pressure and low-pressure balloon catheters. CDT devices consist of infusion catheters and guidewires designed specifically for thrombolysis. The inferior vena cava filters segment is divided into permanent and retrievable filter types. End users of these devices primarily encompass diagnostic centers and hospitals.

Access The Complete Clot Management Devices Market Report:

https://www.thebusinessresearchcompany.com/report/clot-management-devices-global-market-report

Innovation Trends Accelerating the Clot Management Devices Market

Leading companies in the clot management devices industry are continuously innovating to develop advanced technologies that improve treatment outcomes. One notable advancement is the development of computer-assisted vacuum thrombectomy (CAVT) systems, which are designed for efficient removal of blood clots in conditions like deep vein thrombosis and pulmonary embolism. For instance, in April 2024, Penumbra Inc., a US-based medical device manufacturer, introduced the Lightning Flash 2.0 system. This cutting-edge clot aspiration and vacuum thrombectomy technology offers rapid clot removal with enhanced performance by integrating artificial intelligence and sophisticated engineering. It features advanced imaging and suction capabilities, allowing precise clot extraction tailored to various medical scenarios. Such innovations are helping to raise the standard of care in acute and chronic vascular conditions.

Competitive Landscape and Major Players in the Clot Management Devices Market

The clot management devices market features a range of prominent companies that influence its development and competitive dynamics. Key players include Bayer AG, Abbott Laboratories, Medtronic plc, Boston Scientific Corporation, B. Braun Melsungen AG, Terumo Corporation, Acandis GmbH & Co KG, Cook Medical, Merit Medical Systems Inc., Penumbra Inc., MicroVention Inc., Inari Medical Inc., AngioDynamics Inc., Argon Medical Devices Inc., LeMaitre Vascular Inc., iVascular SLU, Straub Medical AG, Rapid Medical, C.R. Bard Inc., and InspireMD Inc. These industry leaders are actively investing in research and development to maintain their market positions and meet evolving clinical needs.

Geographical Market Insights Highlighting Regional Growth Patterns

In 2025, North America held the largest share of the clot management devices market, driven by advanced healthcare infrastructure and widespread adoption of innovative therapies. Meanwhile, the Asia-Pacific region is expected to experience the fastest growth during the forecast period, fueled by increasing healthcare investments, expanding patient populations, and improving access to advanced medical technologies. Other regions covered in the market analysis include South East Asia, Western Europe, Eastern Europe, South America, the Middle East, and Africa, offering a comprehensive view of global market dynamics.

Get in touch with us:

The Business Research Company: https://www.thebusinessresearchcompany.com/

Americas: +1 310-496-7795

Asia: +44 7882 955267 & +91 8897263534

Europe: +44 7882 955267

Email us at: marketing@tbrc.info

Follow us on:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model