Gastrointestinal Devices Market Expansion Is Reshaping Competitive Dynamics Across The Industry

Enhanced with market attractiveness analysis, total addressable market evaluation, company benchmarking matrices, interactive Excel dashboards, expanded supply chain intelligence, emerging startup coverage, and detailed product insights, The Business Research Company’s 2026 market reports deliver more actionable and strategically valuable research.

The gastrointestinal devices market is experiencing significant growth, driven by advances in technology and the rising incidence of digestive system disorders worldwide. This sector plays a crucial role in diagnosing and treating gastrointestinal diseases, making it an essential part of modern healthcare. Below, we explore the market’s current size, the factors fueling its expansion, key segments, trends shaping its evolution, leading companies, and regional insights.

Gastrointestinal Devices Market Size and Projected Growth

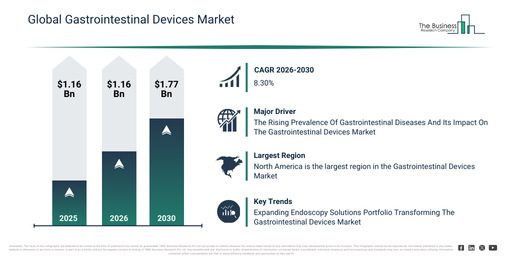

The market for gastrointestinal devices has witnessed solid growth in recent years. From a valuation of $11.7 billion in 2025, it is expected to reach $12.69 billion in 2026, growing at a compound annual growth rate (CAGR) of 8.5%. This historic growth has been fueled by the increasing prevalence of gastrointestinal disorders, expansion of hospital gastroenterology departments, improvements in endoscopic imaging technology, more widespread screening programs, and greater availability of advanced GI devices. Looking ahead, the market is projected to expand robustly, reaching $17.46 billion by 2030 with a CAGR of 8.3%. Key drivers for this anticipated growth include the rising use of AI-assisted GI diagnostics, growing investments in advanced endoscopy centers, the increasing frequency of outpatient GI procedures, demand for single-use GI devices, and a heightened focus on patient safety and procedural efficiency. Additionally, trends such as the rise in advanced GI endoscopic techniques, adoption of capsule endoscopy systems, preference for minimally invasive treatments, expansion of therapeutic endoscopy applications, and enhanced early disease detection tools are shaping market dynamics.

Download A Free Sample Report For Comprehensive Market Insights:

https://www.thebusinessresearchcompany.com/sample.aspx?id=3292&type=smp

Main Factors Propelling Demand in the Gastrointestinal Devices Market

One of the primary forces behind the gastrointestinal devices market growth is the increasing prevalence of gastrointestinal diseases. These disorders affect the digestive tract and related organs, resulting in symptoms that range from mild discomfort to severe health complications. The rise in these conditions is significantly influenced by aging populations, as older adults experience higher rates of digestive system ailments requiring medical intervention. This growing patient base leads to increased demand for specialized diagnostic and therapeutic devices that help healthcare providers manage these illnesses more effectively.

To illustrate this trend, Crohn’s and Colitis Canada reported in July 2023 that the number of inflammatory bowel disease (IBD) sufferers in Canada is expected to rise from approximately 322,600 in 2023 to 470,000 by 2035. This surge clearly highlights how increased disease prevalence is pushing the demand for gastrointestinal devices.

Access The Complete Gastrointestinal Devices Market Report:

https://www.thebusinessresearchcompany.com/report/gastrointestinal-devices-global-market-report

Breakdown of Key Segments in the Gastrointestinal Devices Market

The gastrointestinal devices market is segmented into several categories to better understand its scope and growth areas. By product type, the market includes GI videoscopes, biopsy devices, endoscopic retrograde cholangiopancreatography (ERCP) devices, capsule endoscopy systems, endoscopic ultrasound tools, endoscopic mucosal resection (EMR) devices, hemostasis devices, and other related products. Sales channels consist of online retailing and medical stores including brand outlets. End users are classified as hospitals, clinics and dialysis centers, and ambulatory surgical centers.

Further subcategories include types of GI videoscopes, such as flexible and rigid types; biopsy devices like needle, forceps, and punch biopsy tools; ERCP components including cannulas, guidewires, and balloon sweep devices; capsule endoscopes targeting the small intestine, esophagus, and colon; endoscopic ultrasound with scopes and fine-needle aspiration devices; EMR kits and suction tools; hemostasis devices divided into mechanical, thermal, and chemical agents; and other products including enteral feeding devices and gastrostomy tubes.

Innovations and Trends Influencing the Gastrointestinal Devices Market

Leading companies in the gastrointestinal devices sector are focusing heavily on broadening their portfolios of endoscopy solutions to stay competitive. Expanding these portfolios means introducing new products and services designed to enhance diagnostic and therapeutic capabilities in GI care. Endoscopy, which involves using flexible or rigid tubular instruments to examine the interior of the body, remains central to this innovation.

For example, in January 2023, Fujifilm India Private Limited launched new endoscopy products called ClutchCutter and FlushKnife, which target therapeutic gastrointestinal applications. The ClutchCutter is a rotatable forceps that combines coagulation, dissection, and incision functions in a single device. It features an insulated outer edge for durability and serrated jaws for better grip. The FlushKnife is a diathermic slitter that enables a range of tasks including marking, flushing, incising, dissecting, and coagulation, offering a ball-tip option for enhanced precision in tissue dissection and coagulation.

Key Players Leading the Gastrointestinal Devices Market

The gastrointestinal devices market features several prominent companies that drive innovation and competition. Notable players include B. Braun Melsungen AG, Olympus Corporation, Interscope Inc., Steris plc, Cook Group Incorporated, MICRO-TECH Co. Ltd., Cantel Medical Corp., CONMED Corporation, PENTAX Medical Company, Karl Storz SE & Co. KG, US Endoscopy Inc., Richard Wolf GmbH, Motus GI Holdings Inc., Congentix Medical Inc., ERBE Elektromedizin GmbH, Creo Medical Group plc, GI Dynamics Inc., Mauna Kea Technologies SA, EndoMaster Pte Ltd., and Fujifilm Holdings Corporation.

Regional Distribution and Market Leadership in Gastrointestinal Devices

In 2025, North America held the largest market share in gastrointestinal devices, supported by robust healthcare infrastructure and high adoption of advanced technologies. The Asia-Pacific region ranked as the second largest market, showing strong potential for growth due to rising healthcare investments and increasing awareness of gastrointestinal health. Other regions covered in the analysis include South East Asia, Western Europe, Eastern Europe, South America, the Middle East, and Africa, each contributing to the global landscape of this expanding market.

Get in touch with us:

The Business Research Company: https://www.thebusinessresearchcompany.com/

Americas: +1 310-496-7795

Asia: +44 7882 955267 & +91 8897263534

Europe: +44 7882 955267

Email us at: marketing@tbrc.info

Follow us on:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model