Point-of-Care (POC) Coagulation Testing Market Expansion Is Reshaping Competitive Dynamics Across The Industry

Delivering more actionable and strategically valuable research, The Business Research Company’s 2026 market reports feature market attractiveness analysis, total addressable market evaluation, company benchmarking matrices, interactive Excel dashboards, expanded supply chain intelligence, emerging startup coverage, and detailed product insights.

The market for point-of-care (POC) coagulation testing has been steadily advancing, driven by increasing healthcare demands and technological progress. As medical facilities and patients seek quicker and more accurate coagulation results, this sector is positioned for continuous growth. Below we explore the market size, key factors influencing expansion, major players, and emerging trends shaping the future of POC coagulation testing.

Current and Projected Market Size of the Point-of-Care Coagulation Testing Market

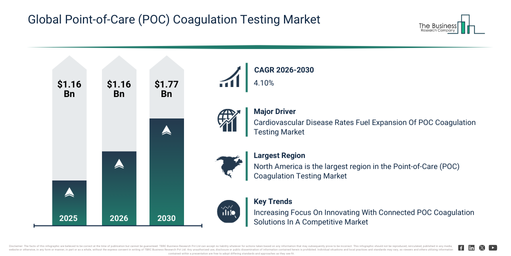

The point-of-care coagulation testing market has experienced consistent growth in recent years. It is projected to rise from $1.25 billion in 2025 to $1.3 billion in 2026, reflecting a compound annual growth rate (CAGR) of 4.2%. This upward trend during the historical period is largely due to the increasing prevalence of cardiovascular diseases that require anticoagulation therapy, as well as heightened demand for rapid coagulation results in settings such as operating rooms and intensive care units. Early adoption of optical and mechanical POC testing technologies and the expanding use of coagulation monitoring across hospitals and clinics have also contributed to growth, alongside broader awareness of point-of-care diagnostics for optimizing treatment.

Download A Free Sample Report For Comprehensive Market Insights:

https://www.thebusinessresearchcompany.com/sample.aspx?id=13913&type=smp

Looking ahead, the market is expected to continue its steady climb, reaching $1.52 billion by 2030, with a CAGR of 4.1%. Factors driving this forecasted growth include a shift towards decentralized and home-based coagulation monitoring, rising adoption of electrochemical detection methods, increased procedural volumes in emergency and trauma care, and wider accessibility through retail and direct tender distribution channels. Additionally, there is growing emphasis on minimizing turnaround times and improving therapeutic outcomes. Key trends likely to shape the market involve expanded use of rapid bedside coagulation testing in critical care, greater reliance on POC devices for anticoagulation therapy monitoring, preference for portable and handheld analyzers, and increasing deployment of coagulation testing in home and outpatient care settings. Demand for real-time clinical decision support through near-patient testing is also on the rise.

Rising Cardiovascular Disease Rates Spur Growth in POC Coagulation Testing

One of the primary forces behind the POC coagulation testing market’s expansion is the escalating incidence of cardiovascular diseases (CVDs). These disorders encompass conditions affecting the heart and blood vessels, such as coronary heart disease, cerebrovascular disease, and peripheral arterial disease. POC coagulation testing plays a critical role in managing CVDs by providing instantaneous data on coagulation status, which aids clinicians in making timely decisions regarding anticoagulation interventions and helps reduce bleeding complications following cardiac surgeries. To illustrate, the Centers for Disease Control and Prevention reported in October 2024 that in 2023, approximately one in six cardiovascular disease fatalities involved adults under 65 years old, with a total of 919,032 deaths attributed to CVD—accounting for one in every three deaths in the United States. This significant burden of cardiovascular disease is a vital driver fueling demand in the point-of-care coagulation testing market.

Access The Complete Point-of-Care (POC) Coagulation Testing Market Report:

Point-of-Care Coagulation Testing Market Segmentation by Technology and End Users

This report segments the point-of-care coagulation testing market based on technology types, distribution channels, and end-user categories. The technology segment includes Optical Technology, Mechanical Technology, and Electrochemical Technology. Optical Technology is further broken down into reflectance photometry, fluorescence detection, and colorimetric detection. Mechanical Technology subcategories include mechanical oscillation and ultrasonic detection. Electrochemical Technology comprises amperometric detection, potentiometric detection, and conductometric detection methods. Distribution channels are classified into direct tenders and retail. End users are segmented into hospitals, clinics, and home care settings, reflecting the diverse environments where POC coagulation testing is utilized.

Collaborations and Innovations Driving Market Advances in POC Coagulation Testing

Key players in the POC coagulation testing sector are investing heavily in developing connected and integrated testing solutions through strategic partnerships. Such collaborations enable companies to combine expertise and technologies to accelerate innovation and enhance competitive positioning. For example, in January 2023, Jana Care, a U.S.-based biomarker assay developer, partnered with Roche Diagnostics of Switzerland. Their joint effort focuses on creating and distributing a point-of-care blood testing platform aimed at screening for chronic kidney disease and heart failure. This cutting-edge system empowers patients to conduct blood tests at home, with data remotely reviewed by healthcare providers, illustrating how technology and collaboration are expanding the reach and convenience of POC diagnostics.

Competitive Landscape Featuring Leading Companies in the Market

The point-of-care coagulation testing market is dominated by several well-established companies. Some of the major players include Siemens Healthcare GmbH, Abbott Laboratories, F. Hoffmann-La Roche Ltd., Danaher Corporation, Sysmex Corporation, IDEXX Laboratories Inc., Quidel Corporation, Werfen SA, Nihon Kohden Corporation, Horiba Ltd., Hycel, Nova Biomedical Corporation, Haemonetics Corporation, Maccura Biotechnology Co. Ltd., Helena Laboratories Corporation, Abaxis Inc., ARKRAY Inc., Radiometer Medical ApS, HemoSonics LLC, iLine Microsystems SL, Corgenix Medical Corporation, Quotient Limited, Micropoint Bioscience Inc., Beijing Succeeder Technology Inc., and EKF Diagnostics Holdings plc. These organizations continue to innovate and compete through product development, partnerships, and expanding global footprints.

Geographical Market Insights Highlighting Regional Leadership

In terms of regional market share, North America led the point-of-care coagulation testing market in 2025. The report covers other critical regions including Asia-Pacific, South East Asia, Western Europe, Eastern Europe, South America, the Middle East, and Africa, providing a global perspective on market dynamics. While North America currently holds the largest share, emerging markets in Asia-Pacific and other regions are expected to contribute significantly to future growth, driven by rising healthcare infrastructure investments and increasing adoption of POC testing technologies worldwide.

Get in touch with us:

The Business Research Company: https://www.thebusinessresearchcompany.com/

Americas: +1 310-496-7795

Asia: +44 7882 955267 & +91 8897263534

Europe: +44 7882 955267

Email us at: marketing@tbrc.info

Follow us on:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model